A New Era of Mortgage Credit Scoring

Nonconforming mortgages are those that do not meet the underwriting standards of government-sponsored enterprises (GSEs) like Fannie Mae and Freddie Mac. While the size of the loan is the most common reason, there are a number of borrower-, property- and structure-specific factors that can push a mortgage into this bucket. Nonconforming loans are generally considered riskier for lenders and thus tend to carry higher interest rates than conforming loans.

Nonconforming mortgage originations (excluding jumbo loans) as a share of all mortgages has doubled over the past three years to reach levels not seen since the 2000s housing crash.1 To help deepen the pool of US consumers eligible for more economical conforming mortgages in the face of pent-up housing demand, the Federal Housing Finance Agency in April expanded underwriting standards for the GSEs to include their first new credit score models in decades: VantageScore 4.0 and FICO Score 10T.

Incorporating additional consumer data like rent-payment history, these models are expected to provide a more complete view of a borrower’s creditworthiness. The GSEs began accepting VantageScore 4.0 through a limited rollout to approved lenders in late April, and FICO Score 10T is expected to be implemented in the coming months. Classic Fair Issac Corporation (FICO) scores will continue to be accepted as the GSEs transition.2

The share of alternative loans is a small portion of the overall market, but non-qualified mortgages—a cohort that includes a large portion of non-jumbo nonconforming mortgages—have historically been the largest segment of issuance within the non-agency residential mortgage-backed security space. Adoption of these new credit score systems appears to be happening faster than expected and may create refinancing incentives for borrowers, which we believe could weigh on conventional low FICO-specified asset pools. That said, the limited scope of the initial rollout may mitigate the near-term impact.3

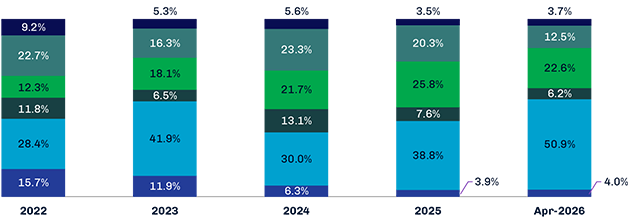

Non-Qualified Mortgages Are the Largest Segment of Non-Agency Issuance

Monthly Non-Agency RMBS Issuance (%)

Source: Deutsche Bank, as of May 1, 2026.

1Source: Inside Mortgage Finance; data as of February 26, 2026.

2Source: Federal Housing Finance Agency; data as of April 22, 2026.

3Source: Asset Securitization Report; data as of May 20, 2026.

The views expressed are those of the author as of May 2026 and are subject to change without notice. These opinions are not intended to be a forecast of future events, a guarantee of future results or investment advice. Investing involves risk, including the possible loss of principal. Past performance is not a guarantee of future results.